Article #469

Last month I warned readers: when the noise gets loud, ignore it; seek advice and wise counsel instead.

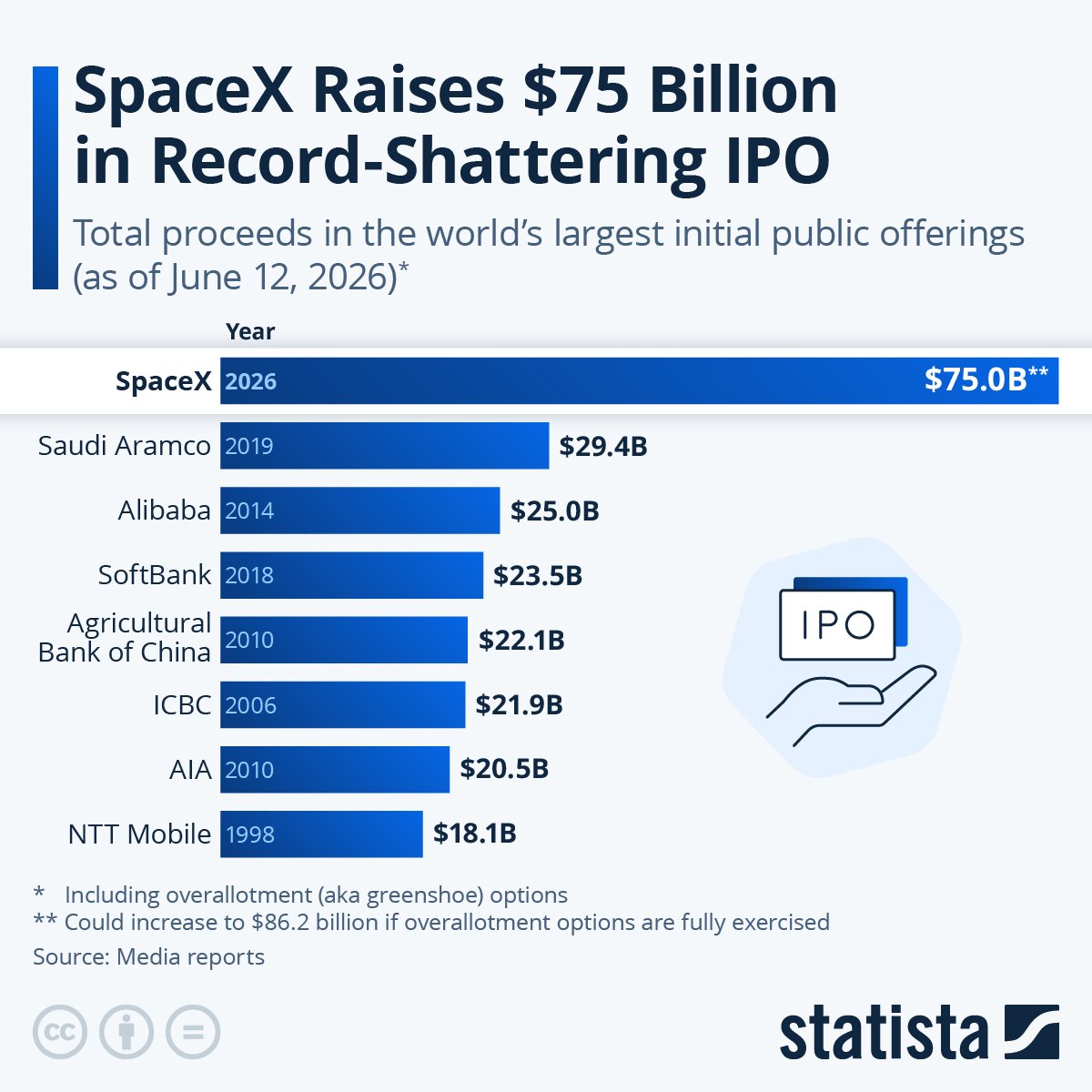

The noise around SpaceX's IPO has been deafening. It priced at USD 135, ripped above USD 225 within days, and briefly made Elon Musk the world's first trillionaire on paper [1]. Then reality hit.

I said the evidence favours patience. Let the froth settle before committing, like a freshly poured beer; you don't drink it while it's all head.

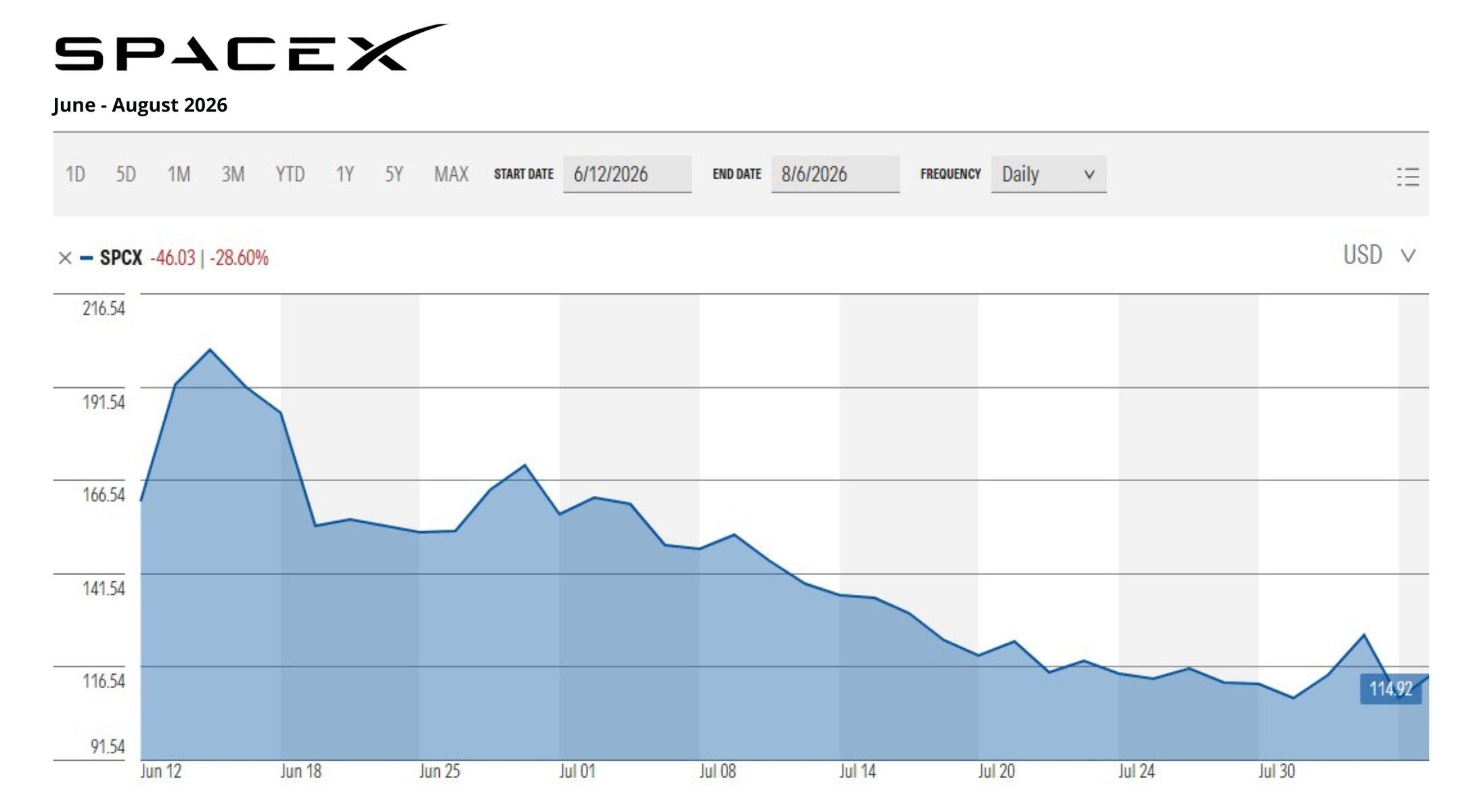

Here's how it settled. SpaceX has crashed straight back to Earth through its own listing price. More than USD 1 trillion, around NZD 1.7 trillion, has been wiped from its value. From a June peak of USD 225 it closed at USD 114.92 on 6th August, below even its USD 135 listing price. Musk's paper fortune has fallen by more than USD 500 billion [1] [2] [3]. The company posted a consolidated net loss of USD 4.9 billion last year, swollen by its xAI acquisition, yet trades at more than 100 times sales [2].

The analysts can’t even agree with one another. Bullish desks pinned targets north of USD 250; HSBC has just opened coverage at USD 115, roughly where it trades; Morningstar reckons fair value sits lower still [2] [3]. When the experts disagree by that margin, you’re not looking at analysis. You’re looking at a story, and stories are priced by mood.

Around 23,000 Kiwis bought in to SpaceX through Sharesies, mostly in the after-market, well after the smart money had taken its seat [1]. By then, the offer-price allocation had happened offshore and the wild ride from USD 135 to USD 225 (and back) was well underway. Those who felt they were getting in early were, in truth, the exit liquidity for those who actually had.

To those investors, I would gently say: none of this is new.

USD 114.92 - SpaceX Closing Share Price on 6th August 2026

Buying for Blue Skies

Our own market taught this very lesson just over a decade ago. You don’t need a crystal ball; only a memory.

In 2014, listings came thick and fast. Travel-software firm Serko and measurement-device maker ikeGPS both floated at $1.10. Both quickly traded below their issue price, with ikeGPS down more than 18 percent on debut [4]. As one fund manager astutely put it: the market had been paying for blue sky three months earlier, and simply wasn't paying anymore [4]. The hype had outrun the businesses. Serko, to its credit, later found real success. Yet even now it trades below the heights the froth once implied, proving that even a ‘good’ company bought at a hyped price can still disappoint for years.

It brings to mind something an old horse trainer once told me: “When they start, they've got the money and I've got the experience; when they leave, I've got their money and they've had the experience.”

News articles on Serko and ikeGPS in 2014

The Quiet Opposite

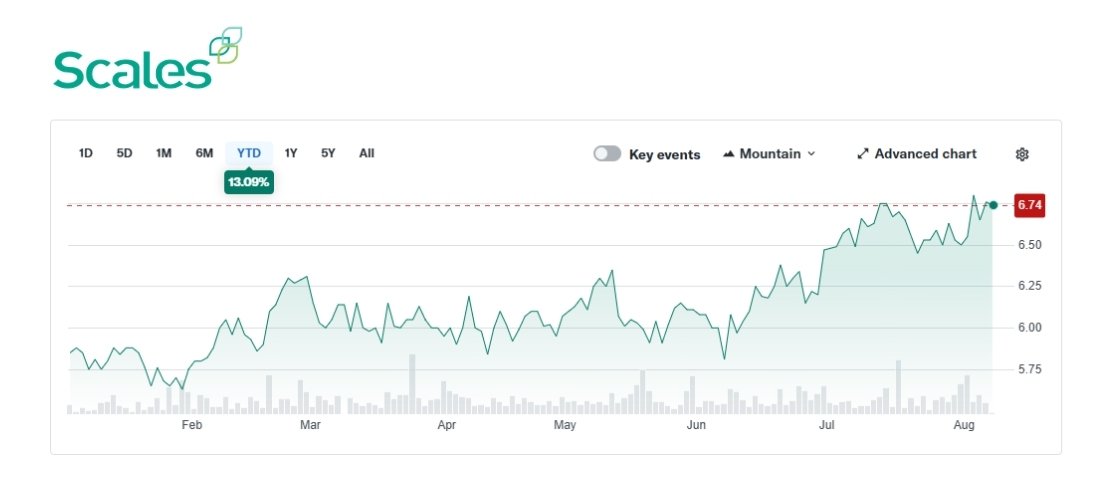

In the same 2014 rush, an old Hawke's Bay apple and logistics business called Scales came to market at $1.60, the very bottom of its indicative range, and had such a subdued debut it too slipped below its offer price in the first few days [5] [6]. No blue sky, no celebrity founders; just apples, coolstores, cargo, with about two-thirds of the business rooted right here in the Bay. Tellingly, the private equity seller kept a 20 percent cornerstone stake rather than bolting for the exit; skin left in the game, not cashed out at the top [6].

IPOs floated by private equity usually attract scepticism, and the inevitable doubters lined up. They were wrong. Net profit came in some 87 percent above the float forecast, and shares today sit near record highs around $6, several times the issue price [7] The overlooked apple grower quietly outran the blue-sky darlings that had stolen the headlines on listing day.

What separates the winners from the wreckage is simple: what you are buying, and who is selling and why. When insiders cash out at the peak, you are not the early investor. You are the exit.

Scales YTD Share Price (December 2025 - August 2026)

The Devil in the Details

There's a sting in the tail many day-one chasers never see coming. It’s buried in fine print, which as I always say, matters more than the selling price.

New Zealand has no general capital gains tax, so most assume share profits are tax-free. Alas, not always. A “stag” buys a float purely to flip on the pop. Buy shares mainly to sell them, and Inland Revenue treats the gain as income, taxed at your rate, up to 39 percent. Buy to hold, and the same shares may not be taxed at all. Intention is everything [8]. Many who chased SpaceX bought the after-market and are now underwater. They’re carrying the flipper's tax intention without the flipper's profit, and are unable to offset the loss.

There's a further wrinkle for anyone with a decent offshore holding. Once your overseas shares pass a cost threshold, proposed to double from NZD 50,000 to NZD 100,000 from the 2026–27 tax year, the foreign investment fund rules can tax a deemed slice of the value each year, whether or not you sold anything [9]. A newer method taxing only realised gains exists, but it is narrow and does not apply to ordinary listed shares like a US-listed SpaceX [9]. These settings are still working through Parliament and turn entirely on your circumstances. None of this is tax advice, but it is exactly the sort of thing you ought to check before you act.

Choosing Patience over Hype

Betting on a day-one pop with no real idea what you own is not investing; it is a coin toss with a tax bill. The alternative is not timidity, and the lesson is not anti-technology. High-growth tech can reward the patient, diversified investor handsomely. It is anti-hype.

A disciplined, evidence-led approach can still be flexible and tactical, positioning around genuine opportunity when the evidence supports it, without chasing froth or mistaking a hyped listing for a considered decision. Scales was the quiet reward for buying a business; the blue-sky floats of Serko and ikeGPS were an expensive lesson in buying a story. SpaceX is that same lesson in a shiny new package.

There is even a footnote of hope for the burned. Facebook fell more than 50 percent below its 2012 float price within four months, then clawed it all back within about fifteen as earnings caught up. A badly priced float can find a floor and recover in time… but that’s cold comfort to whoever paid top dollar on day one, and certainly no substitute for buying well in the first place [3]

When the noise gets loud, the best investors don't chase the rocket. They read the audited accounts, understand who is selling and why, and let time and compounding do the work.

In short: they seek advice and wise counsel. It may behoove others to consider doing the same.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

REFERENCES

1. NZ Herald / Newstalk ZB, "Share crash wipes $1.7 trillion from the value of Elon Musk’s SpaceX, crimps thousands of Kiwi investors" (July 2026)

2. Yahoo Finance, "SpaceX Stock Just Violently Crashed Below Its Opening-Day Price" (July 2026)

3. BeInCrypto, "SpaceX Stock Crash Wipes $500 Billion From Musk’s Fortune" (July 2026)

4. NZ Herald, "ikeGPS plunge may show tech IPO party over" (July 2014)

5. Scoop / BusinessDesk, "Scales shares edge lower on NZX debut" (25 July 2014)

6. NZ Herald, "Scales shares set at bottom of range for IPO" (July 2014)

7. NZ Herald / Direct Capital, "Scales’ Golden Apples"; Stockopedia SCL share data (2026)

8. Inland Revenue, "Share investments": ird.govt.nz

9. Inland Revenue Tax Policy, "Foreign investment fund changes" information sheet (May 2026); Budget 2026 FIF threshold proposal