Article #455

Over 2,400 years ago, the Greek philosopher Plato introduced The Allegory of the Cave in his work The Republic. It told a story of prisoners chained inside a cave, staring at shadows on a wall, convinced that what they could see was all there was to know.

The shadows were cast by objects carried in front of a fire behind them. The prisoners had never seen the real objects, never felt the sun, never experienced the world beyond those flickering shapes on the stone. To them, the shadows weren’t a pale imitation of reality. They were reality. Naming the shadows, predicting their movements, debating their meaning; this was the highest form of knowledge available.

One prisoner escapes. He stumbles out into sunlight, is temporarily blinded, and slowly begins to see the world as it actually is.

Trees. Sky. Colour. Truth.

When he returns to share what he’s found, the others don’t celebrate him. They think he’s lost the plot. They’d rather trust the shadows they know than a reality they can’t yet see.

It’s one of the most enduring metaphors in philosophy. And when I look at how many investors still approach markets today, I can’t help but think of that cave.

The evidence has left the building

The debate between active and passive investing isn’t really a debate anymore, at least not among those who’ve looked at the data.

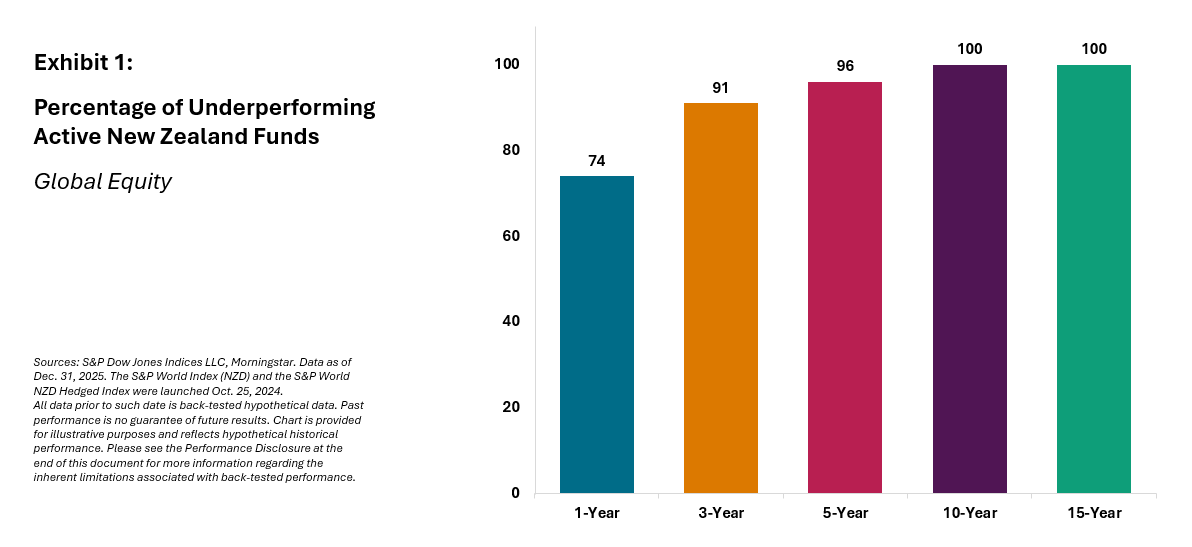

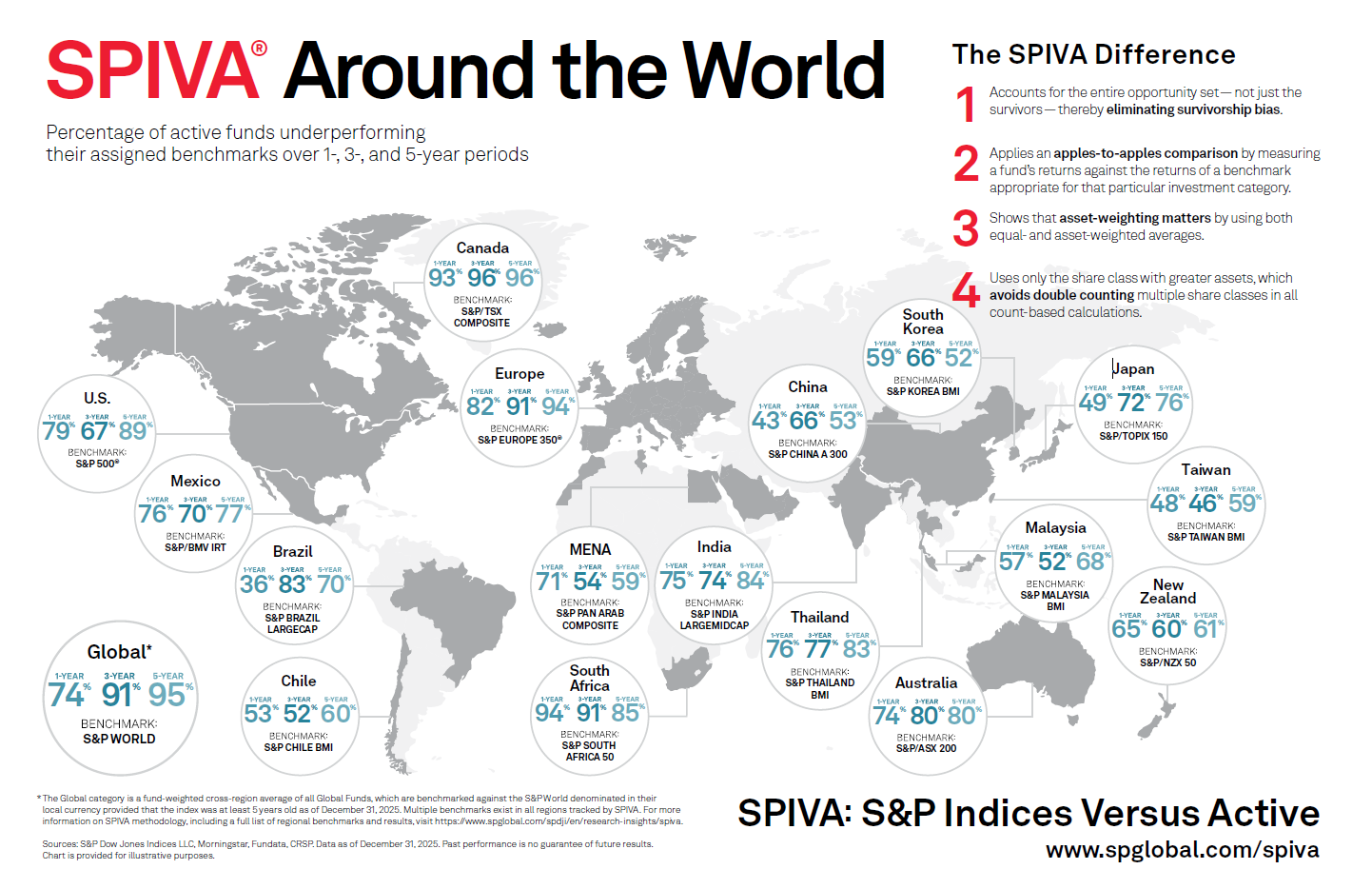

Active investing is the idea that a skilled broker can consistently pick winning stocks and time the market better than the market itself. This has been studied exhaustively, and the results are not flattering. The latest SPIVA New Zealand Scorecard (S&P Dow Jones Indices, April 2026) found 74% of New Zealand’s actively managed global equity funds underperformed the S&P World Index over the 2025 calendar year. Over 10-year and 15-year periods, that figure climbed to 100%.

Every single active global equity fund in this country failed to beat the index over those longer time horizons. Not one outperformed.

The story isn’t much better in domestic markets: 65% of actively managed New Zealand equity funds fell short of the NZX50 last year. Over 15 years, 85% failed to beat it. And in a notable departure from recent trends, 79% of New Zealand bond funds also underperformed in 2025, breaking a four-year run of majority outperformance.

Click image to enlarge

This isn’t a bad year or an anomaly. It’s a pattern that has repeated itself across decades, geographies, and market conditions. Bull markets, bear markets, volatile markets; in each environment, the same story plays out. The majority of active managers, after fees, fall short. And the ones who don’t? Research consistently shows that past outperformance has almost no predictive value for future outperformance. Last decade’s star fund manager is, more often than not, this decade’s cautionary tale.

There’s a popular argument that active managers should shine in turbulent markets — that this is exactly when their expertise should earn its keep. The evidence says the opposite. International research covering 16 countries has found that equity funds tend to underperform during recessions, in part because managers trade more aggressively when conditions get rough, and the elevated trading and liquidity costs in stressed markets eat into whatever edge their stock-picking might have produced. When markets feel chaotic, active managers don’t suddenly become more valuable. If anything, they become more expensive.

Structured, evidence-based investing – using low-cost, diversified funds that capture market returns systematically – has decades of academic research behind it. Eugene Fama won a Nobel Prize in Economics in 2013 for his work on efficient markets. His research, along with that of his colleague Kenneth French, demonstrated that markets are remarkably good at pricing available information, making it extraordinarily difficult to consistently exploit mispricing for gain.

The science is settled in the same way that nutrition science tells us vegetables are better than chips. You can argue with it, but the evidence isn’t going anywhere.

So why do so many investors still choose the shadows?

Back to Plato, because here’s where it gets interesting: the prisoners in the cave weren’t stupid. They just hadn’t seen anything different. The shadows were familiar. Comfortable, and predictable in their own strange way.

Active investing feels like it should work. It’s intuitive. Surely a skilled broker with Bloomberg terminals, decades of experience, and a team of analysts can outsmart the market? Surely timing matters – getting out before the crash, getting back in at the bottom? Surely paying more gets you more?

It feels right. But it just isn’t.

Our own psychology works against us. We humans are wired to believe that effort produces results, expertise commands outcomes, and paying a premium signals quality. These instincts serve us well in most areas of life, yet in investing they routinely lead us astray. We remember the fund manager who called the 2008 crash; we don’t remember the nine who also made bold predictions that year and got it wrong. And we celebrate skill, where luck is the more honest explanation.

The financial media reinforces this. Every week there’s a new “hot fund,” a manager who called the last downturn, a stock tip dressed up as insight. Financial news often exists not to inform investors but to entertain them; to create the impression of a world where markets can be read, timed, and beaten by those clever and bold enough to try. This keeps investors glued to the shadows on the wall, convinced they’re watching something real and meaningful.

The cost of staying in the cave

Beyond philosophy, choosing high-fee active management over a structured, low-cost approach has a very real dollar cost over time. Compounding works both ways: returns compound up, but fees and underperformance compound down. The difference between a 1% annual fee and a 0.35% annual fee might sound trivial. Over a 30-year investment horizon, it can amount to hundreds of thousands of dollars — money that should be in your retirement, not paying for someone else’s.

For New Zealanders building KiwiSaver balances, investment portfolios, or retirement nest eggs, that gap matters enormously. We’re a nation of relatively recent investors, still developing our financial literacy and our instincts around what good advice and good investment management looks like. The cave is particularly dark here, and the shadows particularly convincing, because we haven’t yet had generations of experience to learn from.

The good news is that awareness is growing. KiwiSaver has brought millions of New Zealanders into contact with investment for the first time. The questions being asked are getting sharper. Investors are increasingly curious about what they’re paying, what they’re getting, and whether there’s a better way.

The light is there if you look for it

The exit from the cave is well-signposted. Evidence-based investing isn’t complicated or exotic. It involves owning broadly diversified, low-cost funds, staying invested through volatility, and tuning out the noise. It requires discipline over drama, and patience over prediction.

It also helps enormously to work with the right kind of adviser; one who operates on a fee-only basis, meaning they’re paid directly by you rather than through commissions or product incentives. And one who acts as a fiduciary: legally and ethically obligated to put your interests first. Not their own, and not their firm’s interests – yours, always. In New Zealand that combination is rarer than it should be – but it exists, and it matters more than most investors realise.

Think of it this way… even the prisoner who escapes the cave benefits from a guide who’s already seen the sunlight.

Some investors will make that journey. Some won’t. Not because they can’t, but because the cave is familiar and the light is initially uncomfortable. Change requires admitting that what you believed before may not have served you well. That’s never easy.

A good financial adviser’s job isn’t to drag anyone out blinking into the sunlight. But it is to make sure you know the door exists — and that you don’t have to navigate it alone or pay someone whose interests don’t align with yours to show you the way.

The shadows on the wall were never the whole story.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

REFERENCES

1. S&P Dow Jones Indices. SPIVA New Zealand Year-End 2025 Scorecard. Released April 2026. Key findings: 74% of NZ active global equity funds underperformed the S&P World Index in 2025; 100% underperformed over 10- and 15-year horizons; 65% of NZ equity funds underperformed the NZX50 in 2025 (85% over 15 years); 79% of NZ bond funds underperformed. spglobal.com/spdji

2. Edmunds, S. (28 April 2026). All active funds ‘underperform’ over past year, data shows. RNZ News. rnz.co.nz/news/business/593570

3. Fink, J., Raatz, K., & Weigert, F. Mutual fund performance during recessions (cited via RNZ, April 2026). 16-country study finding equity funds underperform during recessions by approximately 0.4% per month on average.

4. Plato. The Republic (c. 375 BC). ‘Allegory of the Cave’, Book VII. Translated by Benjamin Jowett. Project Gutenberg: gutenberg.org

5. Fama, E.F. (1970). ‘Efficient Capital Markets: A Review of Theory and Empirical Work.’ Journal of Finance, 25(2), pp.383–417.

6. Fama, E.F. & French, K.R. (1993). ‘Common Risk Factors in the Returns on Stocks and Bonds.’ Journal of Financial Economics, 33(1), pp.3–56.

7. The Royal Swedish Academy of Sciences (2013). Scientific Background: Understanding Asset Prices, Nobel Prize in Economic Sciences. nobelprize.org

8. Dimensional Fund Advisors. The Case for Evidence-Based Investing. dimensional.com