Article # 463

Private. Special. Exclusive. Three words that do a lot of heavy lifting in finance. They frame private equity and private credit as access and privilege. Yet beneath the velvet-rope marketing sits a familiar set of trade-offs: high fees, illiquidity, and a lack of transparency. For decades that rope kept ordinary investors out. It was quietly removed, and nobody sent a memo.

Historically, these markets belonged to pension funds, endowments and family offices with eight figures to commit and twelve years to wait. Ordinary investors didn't get a seat at the table. They are now being offered one, through KiwiSaver growth funds, UK Long-Term Asset Funds dropped inside tax-advantaged ISAs, and the family trust portfolios they signed off on last year [1]. The FMA confirmed in April that most KiwiSaver providers expect to materially lift their private asset allocations over the next three years, aligning with global investment trends [2]. The industry calls it democratisation. Governments call it unlocking growth.

This week the trend turned local and concrete. Simplicity committed $30 million to a new Kiwi deep tech and health sciences venture fund, becoming a cornerstone investor [3]. The fund holds a small number of early-stage companies, including pre-revenue biotech automating cancer-cell therapy manufacturing. It is not fully funded on day one; it is a capital-call vehicle, drawn down over the life of the fund. The parent is US-headquartered, and the capital base includes migrant investors using it as a pathway to residency. None of that is hidden, and backing clever Kiwi innovation is a perfectly defensible thing to do. But it is a useful reminder of what this asset class is once you look inside the wrapper: a long-dated, illiquid, concentrated bet that you cannot easily value or exit.

About that 40-year outperformance

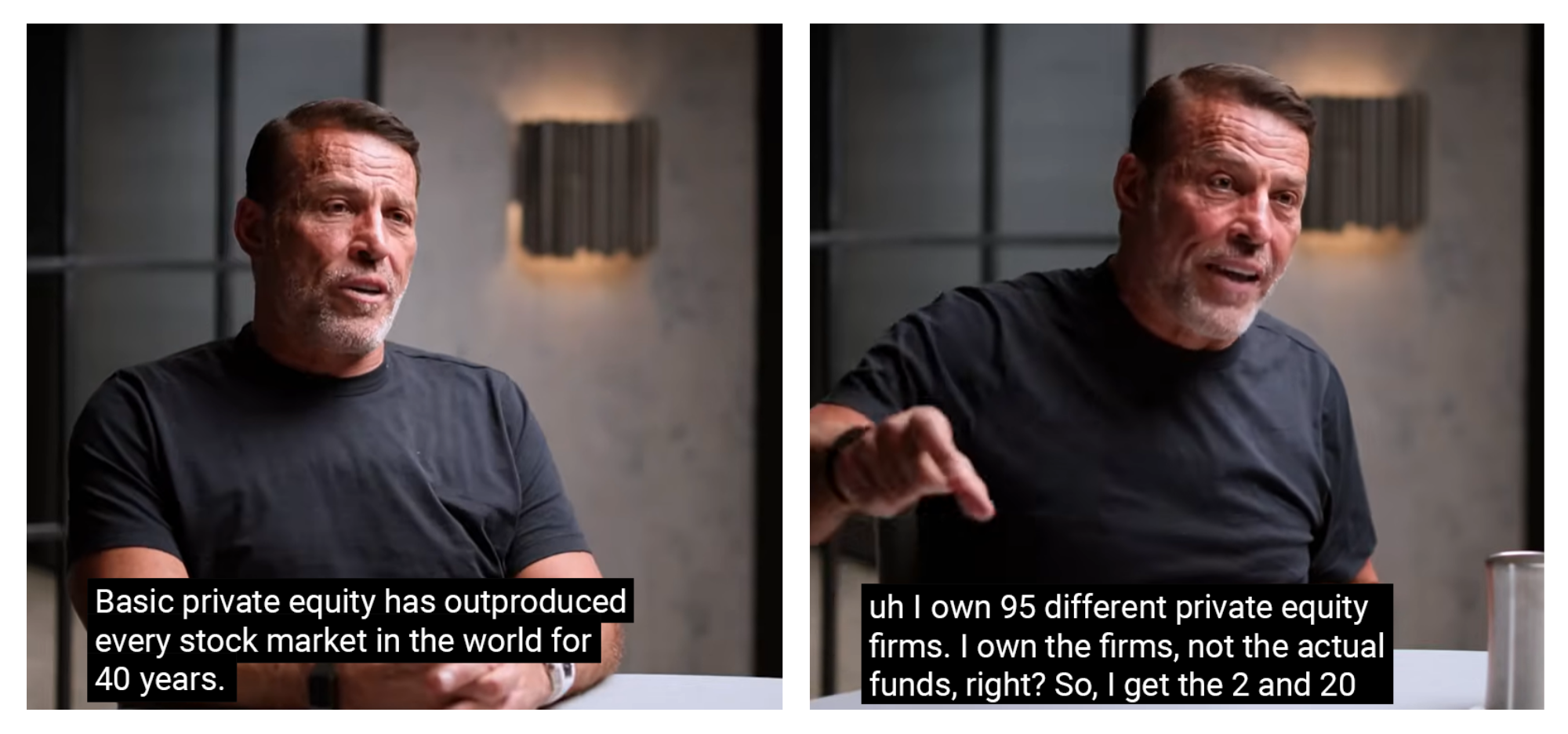

In January, Tony Robbins told millions of viewers on The Diary of a CEO that private equity has outperformed every stock market globally for 40 years, and that ordinary investors have been locked out [4]. He is right on the data. The data, however, deserves a closer look before you remortgage the bach.

First, it has been cherry-picked by survivorship. The funds that blew up quietly drop out of the long-run series, so what you are shown is the record of the survivors, a bit like judging parachutes by interviewing the people who landed. Second, much of the return is leverage, not skill; borrow heavily against a stable business and you amplify the good years, and the bad. Third, and least discussed, is the illiquidity premium. You are tying your money up for a decade or more in a speculative bet on a handful of companies you cannot sell when you want to. You would expect to be paid more for taking on more risk and less liquidity. That extra return is not evidence of genius; it is the rent on your patience. Strip out dead funds, borrowed money and locked-up capital, and the heroic outperformance narrows sharply, and that is before fees [5].

What Robbins is less keen to dwell on is that he co-owns CAZ Investments, which buys stakes in private equity management companies, and that he personally holds stakes in 95 PE firms; the firms themselves, not the funds [6]. He collects the "2 and 20" on each: two percent of assets every year, plus twenty percent of profits above a hurdle [4]. Draw your own conclusions about the shape of those incentives.

The cycle, and the cautionary tale

On the credit side, JPMorgan chief Jamie Dimon used his April shareholder letter to flag what the more enthusiastic salespeople tend to leave in the bag: the credit cycle still exists [7]. Lending standards loosened during the boom. Covenant-lite deals became common in private credit too [8]. When the cycle turns, losses will not stay gated.

In August 2024, the Government placed Du Val Group, an Auckland property developer, into statutory management. This is only the third time that lever has ever been pulled, following Equiticorp in 1989 and Allan Hubbard's vehicles in 2010 [9].

The Du Val Mortgage Fund had been marketed as wholesale-only at around 10% per annum, pitched as comparing favourably to bank term deposits. That label is not a marketing flourish but a regulatory category: an offer made only to wholesale investors is excluded from the disclosure regime built to protect ordinary investors, so there is no product disclosure statement and no entry on the public Disclose register [9]. Roughly 120 to 150 investors are now owed close to $306 million [9]. When investors tried to sue the FMA for failing to protect them, the High Court ruled in Lindeman Investments v FMA that the regulator owes no duty of care to individual wholesale investors [10]. The safety net does not stretch that far, and by design: the wholesale regime switches off most of the retail protections long before any loss is incurred.

Every newborn, a private asset owner

Fisher Funds has committed more than $1 billion of KiwiSaver money to private equity, the largest publicly announced commitment to date [11]. Most other major providers also carry exposure, and per the FMA report most plan to lift those allocations over the next three years [2]. On Sunday, Christopher Luxon announced that, if re-elected, KiwiSaver would become compulsory from 2028, every newborn would be auto-enrolled with a $1,500 Baby Boost defaulted into a high-growth fund, and the combined contribution rate would reach 12% by 2032 [12]. Every newborn New Zealander would begin their financial life with a private asset exposure they did not choose, in a vehicle they cannot exit until at least 2090.

Structure is not the same as transparency

None of this makes private assets an inherently bad asset class. The issue is the layering, the marketing, and the question of who benefits from the door opening now. Where the exposure is plainly structured, a named partnership backing identifiable businesses with disclosed allocations, the picture is more straightforward than where it runs through layered offshore fund-of-funds with opaque manager economics. But structure on paper is not the same as transparency in practice. Diligent managers have tried to look through some of the better-regarded local vehicles and come up short on what is actually held and how it is valued. If the people whose job is to see inside cannot, the ordinary member certainly cannot. We do not invest our own clients in this asset class, for precisely these reasons. It would be premature to suggest New Zealand has quietly cracked private assets when the same transparency, valuation and liquidity questions remain.

Here is what matters most, and what the marketing almost never spells out: understand whether your commitment is fully funded on day one or subject to future capital calls. Some private equity is paid up front, with no further obligation, clean and simple. Much of it is not. A commitment of thirty cents on the dollar today can trigger calls for the remaining seventy cents in the years ahead. Your disclosed allocation now will not reflect your actual exposure tomorrow; as the calls arrive, your percentage holding and your real risk are multiplied. A trustee who signs off on what looks like a modest five percent allocation can find the true commitment is several times that once the fund draws down. I have watched exactly this happen to a community trust, where a decision made by earlier trustees carried obligations that only became visible years later.

For trustees, this is not simply an investment preference; it is a governance question.

Under the Trusts Act 2019, trustees of family and charitable trusts inherit a look-through duty [13]. Few today can name the private asset exposures they are responsible for, let alone the unfunded commitments sitting behind them. Asking the question is the first part of discharging the duty.

Four questions for any provider, adviser, or co-trustee:

What are the all-in fees across every layer?

How are the underlying assets valued: how often, and by whom?

Is the commitment fully funded, or subject to future capital calls?

In whose interest is the allocation being recommended?

The answers should be plain and confident. If they aren't, that itself is a flag you shouldn't ignore.

Robbins is right that private equity has outperformed historically. Dimon is right that the credit cycle still exists. What is less often spoken about is who benefits from unlocking the door now, and why.

Private. Special. Exclusive. Useful words for the fee machine; less useful for the person handing over their money. You are not joining the club; you are funding it.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

We do not hold or advise on any private credit or private equity investments.

REFERENCES

Financial Conduct Authority (UK). Long-Term Asset Fund regime, FCA Handbook COLL 15. HM Treasury (2025). Inclusion of LTAFs in stocks and shares ISAs. gov.uk.

Financial Markets Authority (2026, 15 April). Private assets in managed funds: Investment landscape and valuation practices. Accompanying media release: “FMA anticipates KiwiSaver providers will increase investment in private assets.” Source: FMA.

Simplicity (2026, 24 June). “Simplicity backs ambitious Kiwi innovators with $30m investment.” Details: $30m cornerstone commitment to Bridgewest Venture Fund I (Deep Tech and Health Sciences Fund). Provider disclosure context: Booster, Milford, Generate, Pathfinder, ANZ Investments and others carry private asset allocations across growth and high-growth options.

The Diary of a CEO with Steven Bartlett (2026, 15 January). “Tony Robbins: No One Is Ready For What’s Coming.” Details: transcript references Robbins’ stakes in 95 private equity firms, the firms, not the funds, receiving the “2 and 20” on each.

Bain & Company (2025). Global Private Equity Report 2025. Details: fee conventions of 1–1.5% management plus 10–20% carry above a preferred return. Supporting context: MSCI, Chicago Booth Review and NBER research on buyout outperformance of roughly 3–5% per year over public market equivalents, with debate over the role of leverage, survivorship bias and the illiquidity premium.

CAZ Investments. Firm overview and GP-stakes strategy. Robbins, T., Zook, C. and Mallouk, P. (2024). The Holy Grail of Investing. Simon & Schuster.

JPMorgan Chase & Co. (2026). Annual Letter to Shareholders 2025. Author: Jamie Dimon. Released April 2026. Source: JPMorgan Chase & Co.

Reserve Bank of New Zealand (2026, May). Financial Stability Report. Details: private credit market concerns. Source: Reserve Bank of New Zealand.

Financial Markets Authority (2024, 21 August). “Du Val Group: statutory management ordered.” Source: FMA. Supporting coverage: BusinessDesk (2025, 4 August), “A year since raids, FMA yet to prosecute over Du Val collapse.”

Lindeman Investments Limited v Financial Markets Authority [2025] NZHC. Judgment date: 11 July 2025. Summary source: Cooney Lees Morgan, “The FMA safety net has limits when it comes to wholesale investor groups.”

NZ Herald, The Prosperity Project (2025, 4 August). “The rise of KiwiSaver investing in private equity and what it means for you.” Details: Fisher Funds committing more than $1 billion of KiwiSaver funds to private equity.

New Zealand National Party (2026, 21 June). “National To Further Boost Kiwis’ Financial Security.” Details: press release, annual conference, Lower Hutt. Coverage: NZ Herald, RNZ, 1News, Newsroom and Scoop (21–22 June 2026). Estimated fiscal cost: $1.1 billion over four years.

New Zealand Parliament (2019). Trusts Act 2019, ss 30–31.