Article #453

April 21st marks the anniversary of Manfred von Richthofen's death: the legendary Red Baron who claimed 80 aerial victories before falling at just 25 years old.

Since childhood, I've been captivated by his story. Here was an aerial combat pioneer and crack shot hunter since his youth, who transformed the chaos of dogfighting into a disciplined science. What makes his story relevant for investors isn't his success, but how he achieved it through disciplined adherence to proven principles – and ultimately, how he lost everything by abandoning them in a single moment of exuberance.

From Hunter to Ace

Von Richthofen's foundation as a hunter shaped everything that followed. Before he ever climbed into a cockpit, he'd spent years stalking game on his family's Silesian estate, learning patience, precision, and the critical importance of positioning. A hunter doesn't charge blindly at prey; he studies wind direction, uses terrain for cover, and waits for the perfect shot. Honed since boyhood, these instincts would prove invaluable in the skies above the Western Front.

He brought this hunter’s mentality with him when he transferred to the Imperial German Air Service in 1915. He learnt his craft from Oswald Boelcke, the era's preeminent fighter tactician, whose maxims established fundamental rules for air combat. But von Richthofen didn't simply follow his mentor's teachings; he refined them through his own experience into his own dicta – an effective combat manual that became the foundation for his legendary Flying Circus.

The Dicta: A Hunter's Discipline Applied to Combat

The Baron's rules were precise and probabilistic, each designed to stack advantages systematically.

Secure advantages before attacking: altitude, sun position, numerical superiority. Like a hunter choosing his ground, never engage until the odds favour you.

Attack from behind where opponents can't see you, just as a hunter approaches game from downwind.

Fire only at close range when your target is properly in your sights – ammunition is limited, and wild shots achieve nothing.

Always carry through an attack once started. Half-measures waste the advantage you've worked to secure.

Keep your eye on your opponent; never let them trick you into looking away. A hunter who loses focus on his quarry finds himself suddenly the hunted.

When threatened, don't evade—turn and face the attack. Running reveals your vulnerability; confronting the threat keeps you in control.

Over enemy lines, always remember your line of retreat. Know where safety lies, just as a hunter always knows the path back to camp.

He drilled his pilots in these tactics as they flew, pairing them as leader and wingman, spaced 60 metres abreast to allow room for manoeuvre without collision. They flew in tight formation, massing their power for coordinated strikes. This ensured every engagement began with probability tilted in their favour.

The Flying Circus became legendary for systematic execution. Von Richthofen applied that hunter's patience to aerial warfare, refusing to engage unless conditions favoured him. His bright red Fokker Dr.I triplane was essentially psychological warfare, announcing his presence and unnerving opponents before the first shot was fired.

Manfred von Richthofen (centred) with his mentor Hauptmann Oswald Boelcke (left) and Reserve Lieutenant Max Immelmann (right)

From Nick Stewart’s personal collection

Stacking Structural Advantages in Investing

Just as von Richthofen never attacked without multiple advantages working simultaneously, successful investing requires layering structural advantages that compound over time:

Numerical superiority: Broad diversification reduces unsystematic risk. Rather than betting everything on a single stock or sector, spread exposure across asset classes, geographies, and market capitalisations. You're not dependent on any single position succeeding, giving you better odds overall.

Securing altitude advantage: Tilts towards factors like value and small-cap, which decades of academic research show provide systematic return premiums over time. This means you begin each engagement from a position of structural strength backed by empirical evidence.

Additionally, low costs prevent silent erosion of returns. Every percentage point in fees is altitude surrendered before the engagement begins. Index and enhanced index funds that minimise expenses ensure more of your capital remains invested and compounding rather than being siphoned off.

Remembering your retreat: Liquidity enables repositioning when needed. Like von Richthofen’s strategy, portfolios need the ability to adapt without being trapped in unfavourable positions. Illiquid investments might offer higher returns, but they remove flexibility precisely when you might need it most.

Always see things through: Tax efficiency keeps more capital compounding. In New Zealand's relatively benign capital gains environment, this means strategic timing of realisations, thoughtful use of portfolio investment entities, and attention to income versus capital return characteristics.

Like securing altitude and sun position before attacking, proper asset allocation and positioning come first. Like firing only at close range with targets in your sights, investment decisions require clear conviction based on evidence, not speculation. Like the Flying Circus's coordinated attacks, diversification across asset classes works more effectively than concentrated bets.

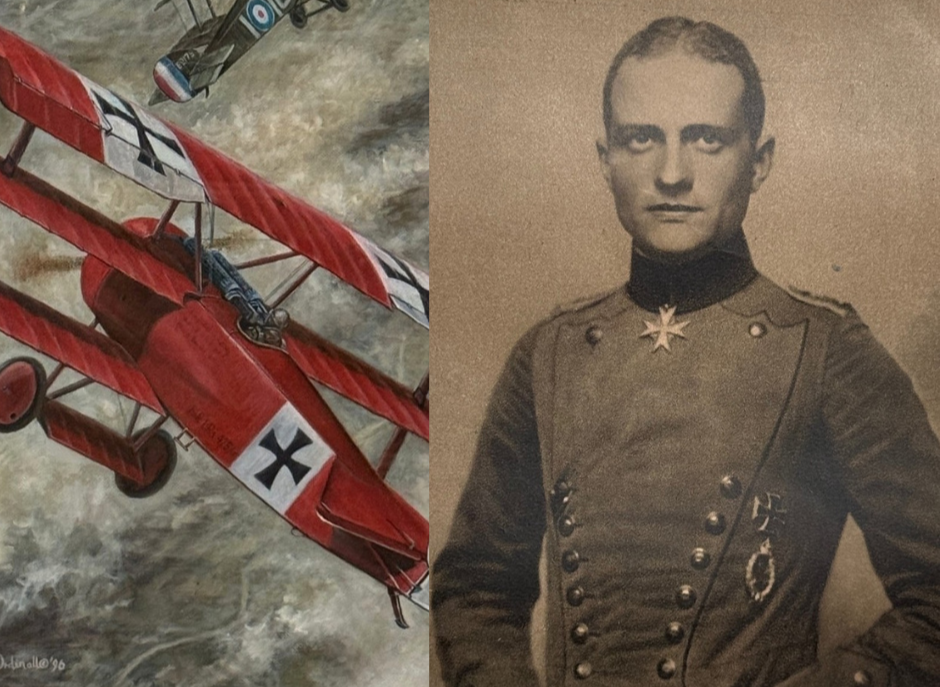

Oil painting by Max Ordinall, from Nick’s personal collection

Constant Awareness: The Discipline of Waiting and Watching

Von Richthofen's rule about keeping your eye on your opponent and never being tricked into looking away speaks directly to behavioural finance. The greatest threat to individual investment success isn't market volatility. It's our own behavioural biases, causing us to look away at critical moments.

In investing, maintaining awareness means monitoring what you can control whilst ignoring what you can’t - AKA the noise designed to distract:

Portfolio drift from target allocations matters. Daily market movements don't.

Rebalancing opportunities when asset classes diverge significantly from targets matter. Quarterly earnings reports for individual companies within diversified index funds don't.

Changes in personal circumstances requiring plan adjustments matter. Predictions about where markets are headed next month don't.

Discipline is harder in practice than in abstract. The retail investment industry generates an overwhelming torrent of information, most of it designed to make you feel you're missing something critical if you're not constantly trading. But as von Richthofen ignored enemy aircraft that didn't present advantageous engagement opportunities, investors must ignore much of market commentary and focus solely on what affects their systematic advantages.

Systematic Execution: Rebalancing as Tactical Discipline

Disciplined rebalancing is your “always carry through an attack once started” parallel. When equity markets surge beyond target allocations, trim them back to target. When they fall and fear is highest, rebalance back into them. Half-measures, like trimming only slightly or delaying rebalancing in case of a better opportunity later, waste the systematic advantage you’ve built.

This is extraordinarily difficult psychologically. Trimming equities after they've surged feels like selling winners. Adding to equities after they've fallen feels like catching a falling knife. But this mechanical adherence removes emotion from decision-making and ensures you're systematically buying low and selling high without attempting to time markets.

Von Richthofen's pilots didn't abort attacks halfway through if conditions looked momentarily unfavourable. They committed fully, trusting their systematic advantages would prevail. The same discipline applies to rebalancing: execute completely. Trust the process.

When Threatened, Face the Attack

When markets plunge, and portfolios decline, every instinct screams to sell, to "preserve what's left”, or to flee to cash.

This is precisely when systematic discipline matters most. Loss aversion—the behavioural bias where losses feel roughly twice as painful as equivalent gains—drives panic selling at market bottoms. Recency bias makes recent volatility feel like the new permanent reality. These biases trick investors into looking away from their long-term objectives and focusing on short-term pain.

Facing the attack means maintaining perspective. Your goals—retirement security, educational funding, legacy objectives—haven't changed because markets had a volatile quarter or year. Your systematic advantages—diversification, factor tilts, low costs—still function. The evidence supporting long-term equity returns hasn't evaporated.

Avoiding Fatal Deviation

The Baron's final flight on April 21, 1918, illustrates what happens when principles are abandoned. Engaging Canadian pilot Wilfrid May in a prolonged dogfight, von Richthofen broke multiple cardinal rules. The wind that day blew from an unusual direction—not the prevailing westerlies favouring German pilots. The extended engagement pushed him progressively deeper over Allied lines near the ridgeline at Corby.

He forgot his line of retreat. Flying low in pursuit of a relatively inexperienced opponent, he'd surrendered altitude advantage for the thrill of another victory. No wingman accompanied him. No formation support protected him. Every systematic advantage that had kept him alive through 80 victories had evaporated in the heat of pursuit.

A single, well-timed shot from Australian ground troops ended the legend—despite the aerial victory subsequently claimed by Canadian RAF pilot Roy Brown. One bullet. One moment of losing sight of position, probability, and principles.

Investors make remarkably similar mistakes constantly. Prolonged bull markets create overconfidence, and carefully constructed asset allocations drift unchecked because "equities always go up" or "bricks and mortar never lose value." A colleague's cryptocurrency windfall makes disciplined portfolios feel inadequate, tempting abandonment of evidence-based strategies for speculation. Market corrections trigger panic selling despite decades until retirement, abandoning the systematic discipline that would mean buying at depressed prices.

These are precisely the moments when abandoning proven principles feels most justified—and when probability turns decisively against us. We're pursuing that one more gain, chasing performance, abandoning our line of retreat.

Von Richthofen's legacy is defined by the systematic, probabilistic approach that made him exceptional – and his demise shows the value in sticking with what works.

His manual endures because it improves probability in combat. Markets require a similarly disciplined approach: following proven principles not just when conditions are favourable, but especially when every instinct says otherwise.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

REFERENCES

Franks, N. & Bennett, A. (1995). The Red Baron's Last Flight. Grub Street Publishing.

Kilduff, P. (2007). Red Baron: The Life and Death of an Ace. David & Charles.

Fama, E.F. & French, K.R. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

Kahneman, D. & Tversky, A. (1979). "Prospect Theory: An Analysis of Decision under Risk." Econometrica, 47(2), 263-291.