Article #461

In August 1602, the Dutch East India Company pinned up posters in Amsterdam announcing that any resident of the Low Countries could buy a share in their new venture. By month's end, 1143 investors had put in roughly 6.4 million guilders. One was a maid named Neeltgen Cornelis. She put in 100 guilders, around half a guilder a day in wages, more than half a year's earnings. The world's first IPO had its first ordinary shareholder.

Four centuries later the dance is the same, but the music is louder. Within 12 months we'll likely see the three largest technology listings in history, landing one after another.

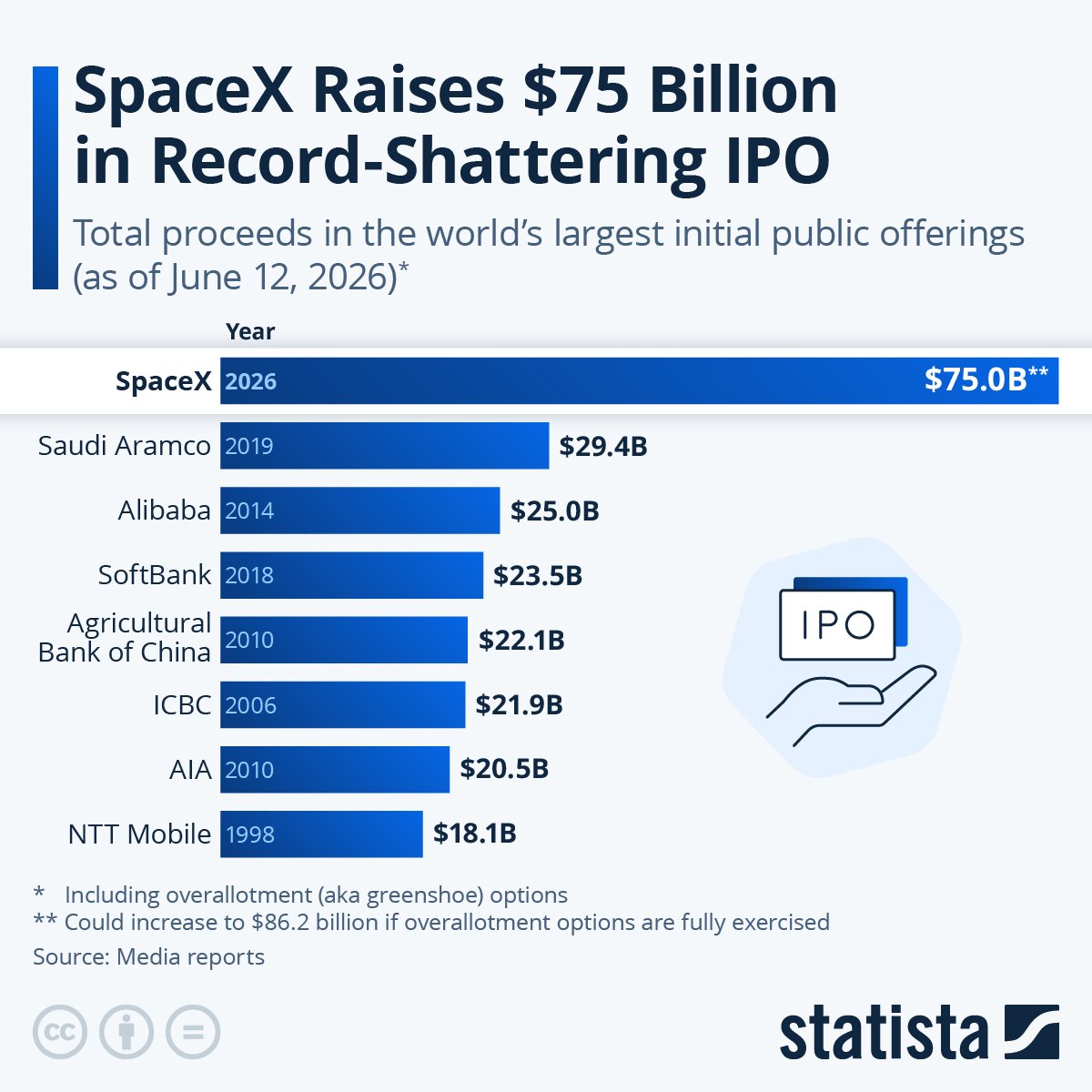

SpaceX lists on the Nasdaq today under SPCX, in what is set to be the largest IPO in history. The company has raised USD 75 billion, pricing 555.6 million shares at USD 135 each, at a valuation approaching USD 2 trillion. For context, the previous record-holder, Saudi Aramco in 2019, raised USD 29.4 billion. Retail orders alone reportedly exceeded USD 100 billion. Elon Musk retains 85 percent of the voting control and stands on the verge of becoming the world's first trillionaire. Roughly 30 percent of the offer has been earmarked for retail through Robinhood, Schwab, Fidelity, E*Trade and SoFi, an unusually generous allocation designed to put ordinary investors at the front of the queue from day one.

The mechanics deserve a look. The raise implies a free float in the low single digits, perhaps three to four percent of the company. The retail offer is distributed through institutions including Goldman Sachs as lead, with Morgan Stanley, Bank of America, Citigroup and JPMorgan in support. Musk's 85 percent voting control comes through a dual-class structure that the New York and California state pension funds have publicly criticised as 'extreme'.

The numbers behind the headline are sobering. SpaceX posted a Q1 2026 net loss of USD 4.3 billion on revenue of USD 4.69 billion. The Connectivity unit (Starlink) made USD 1.19 billion, while the Space unit lost USD 619 million and the AI unit lost USD 2.5 billion.

Starlink is single-handedly carrying the company.

The S-1 also claims a USD 28.5 trillion total addressable market, and includes a vesting condition for 1 billion of Musk's performance shares that requires SpaceX to establish a permanent human colony on Mars with at least 1 million inhabitants. This is a remuneration trigger.

OpenAI is queueing up directly behind. The ChatGPT maker confidentially filed in late May at a USD 852 billion valuation, with Goldman Sachs and Morgan Stanley leading, targeting a September quarter listing. But there is a tell. The Wall Street Journal reports CFO Sarah Friar has told colleagues the company may need more time, while CEO Sam Altman has been eager to push ahead. The CFO, the person responsible for the numbers, is the one urging caution. OpenAI has reportedly missed multiple internal revenue and user targets, and its lead is now under threat from Anthropic, whose tools are being adopted across the workforce at pace. OpenAI is going public partly because it needs to, having committed more than USD 1.4 trillion to physical infrastructure. The phrase 'stolen a charity', used by Musk in the recently dismissed trial alleging OpenAI improperly converted from a nonprofit research lab, will hang over the prospectus regardless of the verdict. Anthropic is preparing its own listing.

Three deals, perhaps USD 200 billion of equity issuance, in a single year. As a fiduciary, not as a fan of rockets or large language models, my answer is the same as it would have been to a client asking about the South Sea Company in 1720. Probably not, and almost certainly not at the open.

The unromantic data

Jay Ritter at the University of Florida, known in finance circles as 'Mr IPO', has been cataloguing initial public offerings since 1980. US IPOs have, on average, trailed the broader market by roughly two percentage points a year over the three years after listing. Almost two thirds underperform.

Dimensional Fund Advisors found the same in a study of more than 6,000 US IPOs from 1991 to 2018. Dimensional's response is instructive. Their funds deliberately wait, sitting out the first year or so after a listing so that the early froth settles, the lock-ups expire, and at least one to two years of audited public-company financials accumulate before they buy. Dull, patient, and on the evidence, profitable.

Read Dimensional’s study HERE.

Two New Zealand parables

We do not have to travel to Starbase, Texas for the lesson. Two recent local listings sit at opposite ends of the IPO spectrum.

Napier Port listed in August 2019 at $2.60 a share, rose sharply on debut, touched $4.28 by year-end, and today trades in the low $3 range with a steady dividend stream. Not spectacular, but it is what a 150-year-old infrastructure business with predictable cargo volumes is supposed to look like. Decades of audited accounts. A board that knew what it owned. A business you can model on the back of an envelope.

My Food Bag tells the other story. It listed in March 2021 at $1.85, the largest New Zealand IPO by amount raised since 2014. The prospectus glittered. Retail investors, including many existing customers, were warmly invited. The shares fell on day one and kept falling. Today they trade around 29 cents, an 85 percent loss for anyone who bought at issue. A classic private equity exit, with the existing owners taking $51 million in repaid shareholder loans and a $7.1 million pre-listing dividend off the table on the way out. The question not asked loudly enough was the only one that mattered: who is selling, and why now?

The fiduciary filter

Three principles we keep returning to when a client asks about a hot IPO. First, wait for the audited financials. The Dimensional approach of holding off until at least two years of statutory accounts exist as a listed entity is not market timing, it is risk management. Pre-IPO numbers are produced under different incentives.

Second, read who is selling. Founders and venture funds with five-year-old positions do not list out of generosity. Lock-up provisions and use of proceeds tell you more than the forward revenue projection. Third, recognise the window. Ritter's research shows IPOs cluster in optimistic markets and underperform most when issued in those hot windows. Three trillion-dollar AI and aerospace deals queued up in a single year is the textbook definition.

And so, to Amsterdam

Neeltgen Cornelis did rather well. The VOC paid its first dividend in 1610, mostly in spices, and continued paying for the better part of two centuries. But she bought into a business with existing ships, warehouses, a 21-year charter and a recognisable revenue model.

She was not buying a million Martians.

The colossal IPOs of 2026 may yet reward their early shareholders handsomely. Some will. Most, on the historical evidence, will not. When the noise gets loud, seek advice and wise counsel.

Or, if you prefer the older formulation - ask the person who has read the prospectus three times and is still not buying.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

REFERENCES

Bloomberg Evening Briefing Americas, 11 June 2026, 'The world's first almost-trillionaire'. SpaceX priced 555.6 million shares at USD 135 each, raising USD 75 billion. Retail orders reportedly exceeded USD 100 billion.

Bloomberg Evening Briefing Americas, 20 May 2026, 'SpaceX Files Publicly for Nasdaq IPO Under Symbol SPCX'.

The Economist, World in Brief, 21 May 2026, 'SpaceX reaches for the stars'.

Morning Brew, 21 May 2026, 'SpaceX shows its finances and future in IPO filing'. SpaceX S-1 prospectus, 20 May 2026: Q1 2026 revenue USD 4.69 billion, net loss USD 4.3 billion; Musk 85 percent voting control; Mars 1 million inhabitants vesting condition; total addressable market claim USD 28.5 trillion; retail distribution via Robinhood, Schwab, Fidelity, E*Trade, SoFi.

BusinessDesk (WSJ syndication), 21 May 2026, 'OpenAI is preparing to file for an IPO very soon'. CFO Sarah Friar reportedly told colleagues OpenAI may need more time; Anthropic growing faster on workforce tool adoption.

CNBC and Wall Street Journal, 20 May 2026, 'OpenAI to confidentially file for IPO as soon as Friday', valuation USD 852 billion.

Ritter, J.R., 'Initial Public Offerings: Underpricing', 1980 to 2025 dataset, University of Florida, Warrington College of Business.

Black, S. and Green, K., 'IPOs: Profiles Are High. What About Returns?', Dimensional Fund Advisors, 2019, study of 6,000+ US IPOs 1991 to 2018.

RNZ, 'Will your My Food Bag investment ever recover?', May 2025.

NZX disclosures, Napier Port Holdings (NPH) and My Food Bag Group (MFB), historical share data.

Worldsfirststockexchange.com, Dutch National Archives, VOC charter 20 March 1602, Article 10.