Okay, this one created quite a stir in financial circles. ANZ Investment Services (New Zealand) decided to stop Bonus Bonds and wind up the investment scheme by the end of October and return funds to bondholders. Here is a thought for those who feel disheartened.

The power of compounding

I hear young people complaining on a regular basis that it’s impossible for them to save money. The list holding them back is a long one – student loans, minimum pay, rent, coffee, and the desire to enjoy their youth.

Small and regular will yield results

If you are 5 or 45 years away from retirement, joining KiwiSaver is a ‘no brainer’ option.

There is the free $1,000 kick-start from the Government, which gets your KiwiSaver savings and compounding returns started immediately; member tax credits for contributing members aged between 18 and 65 years (currently up to a maximum of $521 per member per annum); and if you are over 18 your employer will match your contributions (the minimum now being 3 percent).

KiwiSaver is locked in until 65 meaning unless you use it to buy your first home or suffer hardship. This means that if you continue to contribute to it, your KiwiSaver Scheme Fund will be a nice little nest egg to supplement your NZ Superannuation when you decide to retire.

Other benefits are that you can easily transfer between KiwiSaver providers if you are not satisfied with your current KiwiSaver experience (whether for performance, reporting, change of ownership or other reasons); you can easily switch between funds staying with your same provider, eg from growth to balanced; and if you have lived overseas and have acquired a foreign pension or superannuation fund, you can transfer it into your KiwiSaver Scheme Fund (however, not all countries or KiwiSaver providers will allow transfers).

To simply depict how effective it is to join KiwiSaver:

If you are 20, just finished your tertiary education and earning $30,000, your annual KiwiSaver contribution (at the current minimum rate), will be $900, with your employer also contributing $900.

This will mean by the end of year 1, you will have a KiwiSaver balance of $2,800 without taking into account any growth (or fees). Your 45 years of KiwiSaver contributions, allowing for a 2% increase in salary each year, and an assumed net yield from your investment of 5% per annum, will give you $508,820 by age 65. It is important to note that these calculations do not take into account inflation - $500,000 in 45 years will not have the same spending power as $500,000 does now.

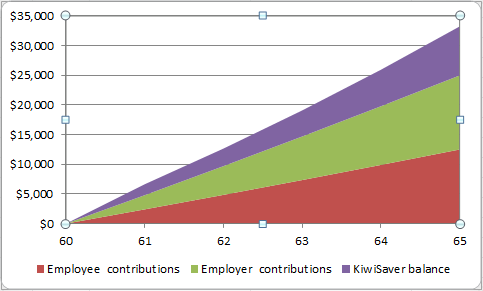

20 Years and above age with 30 K annual earnings

If you are 60, on a $80,000 salary, with 5 years left until NZ Superannuation kicks in, your annual KiwiSaver contribution (at the current minimum rate), will be $2,400, with your employer also contributing $2,400 each year. If we take into account your 5 years of KiwiSaver contributions, again allowing for 2% salary increases and a 5% net yield then you will have $33,229 at retirement age. Or you could up your contributions to the maximum rate of 8 percent with your employer’s still at 3 percent, and your KiwiSaver balance at 65 would be $57,337. Again, inflation is not taken into account in these calculations.

60 years and above with 80 K earnings

It sounds too easy, doesn’t it?

The key is that small and regular contributions make savings happen, and as they grow, the gains you make are re-invested in your KiwiSaver Scheme Fund and have a compounding effect, meaning your KiwiSaver investment gets bigger and bigger. Obviously, the rate of growth of your KiwiSaver investment depends largely on the type of fund you’re invested in which is usually decided by a couple of other factors like your appetite for risk, age and number of years until retirement, which will dictate the type of fund you invest in and the proportion of volatility it is exposed to. For example, a growth fund always has a greater proportion of equities compared to a conservative fund, which will be invested in more fixed interest and less equities. Therefore the growth rate of your KiwiSaver Scheme Fund will depend on how the fund is invested, the fees and if you’re entitled to tax member tax credits.

Meaning, it is never too late to join KiwiSaver and the sooner you start, the more you have to gain when you do decide to retire.

- Source: Outside the Flags, Dimensional Fund Advisers