Article #464

I turned 50 on the second of July. That includes nearly 30 in the workforce, 26 years as a financial adviser, 20 as a husband and 18 as a father. Do the maths and I'm roughly two-thirds through my optimal earning window, if we call 65 the end of the innings. It’s made me stop and do the thing I always ask of clients: take an honest look at where I am now, and where the next 15 years are heading.

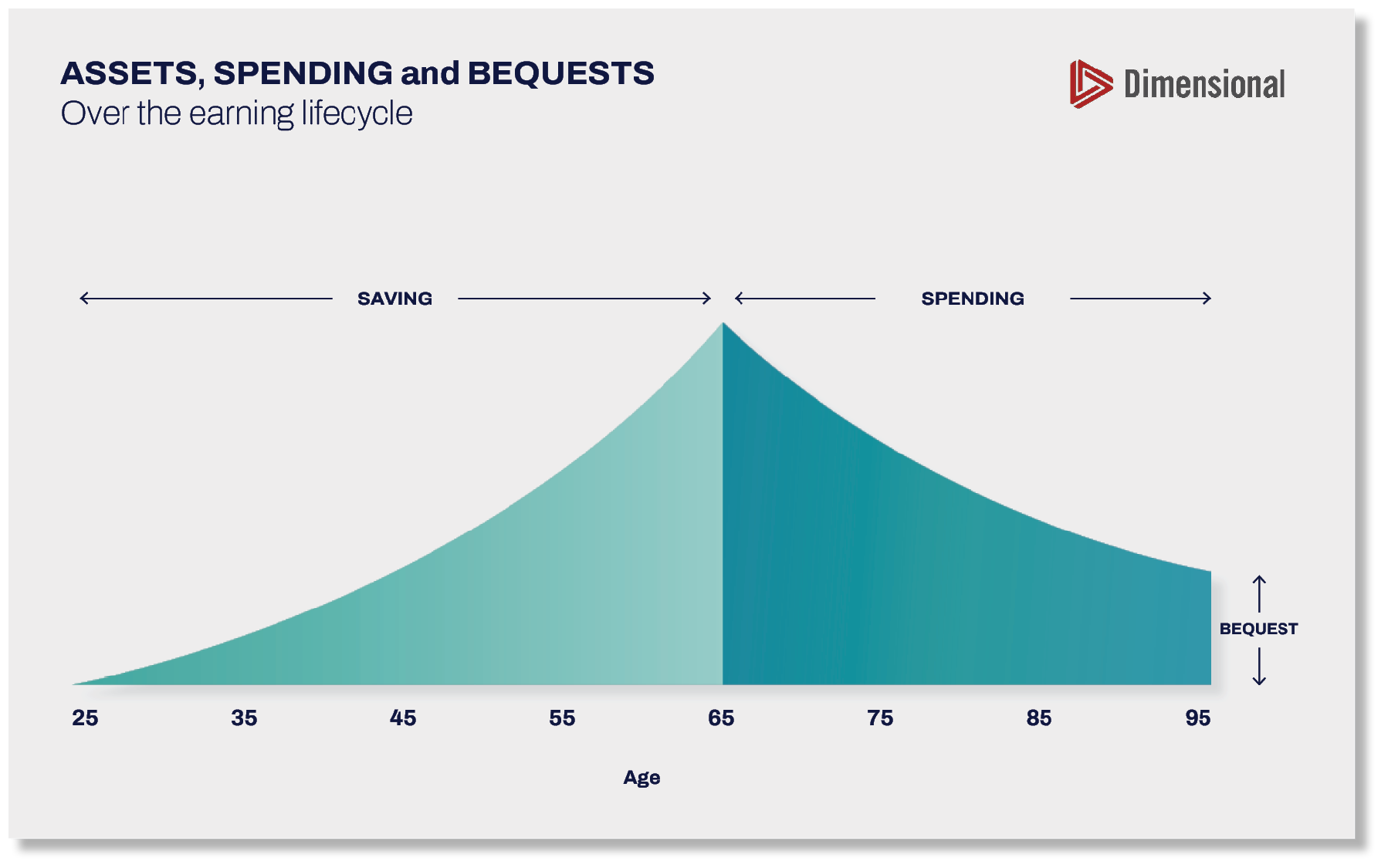

Most of us never think about the shape of our earning life, but it follows a pattern. The 20s are for learning a trade, finding your feet in a profession, perhaps marrying, often still paying off the student loan. The 30s bring children, a mortgage and the long grind of deepening a career. By the 40s the income finally lifts and a little pressure comes off. Then the 50s and 60s arrive, and many people start thinking about the golden years to come. Here’s the rub: a fit and healthy 65-year-old has not just finished their best earning years; for many, the earning stream has stopped altogether. The way we’re living these days, those earnings now need to carry us all the way through to our 90s. That’s three decades of withdrawals from a jar you stopped filling, so you need to put a lot of cookies in that jar to sustain yourself for 30 years.

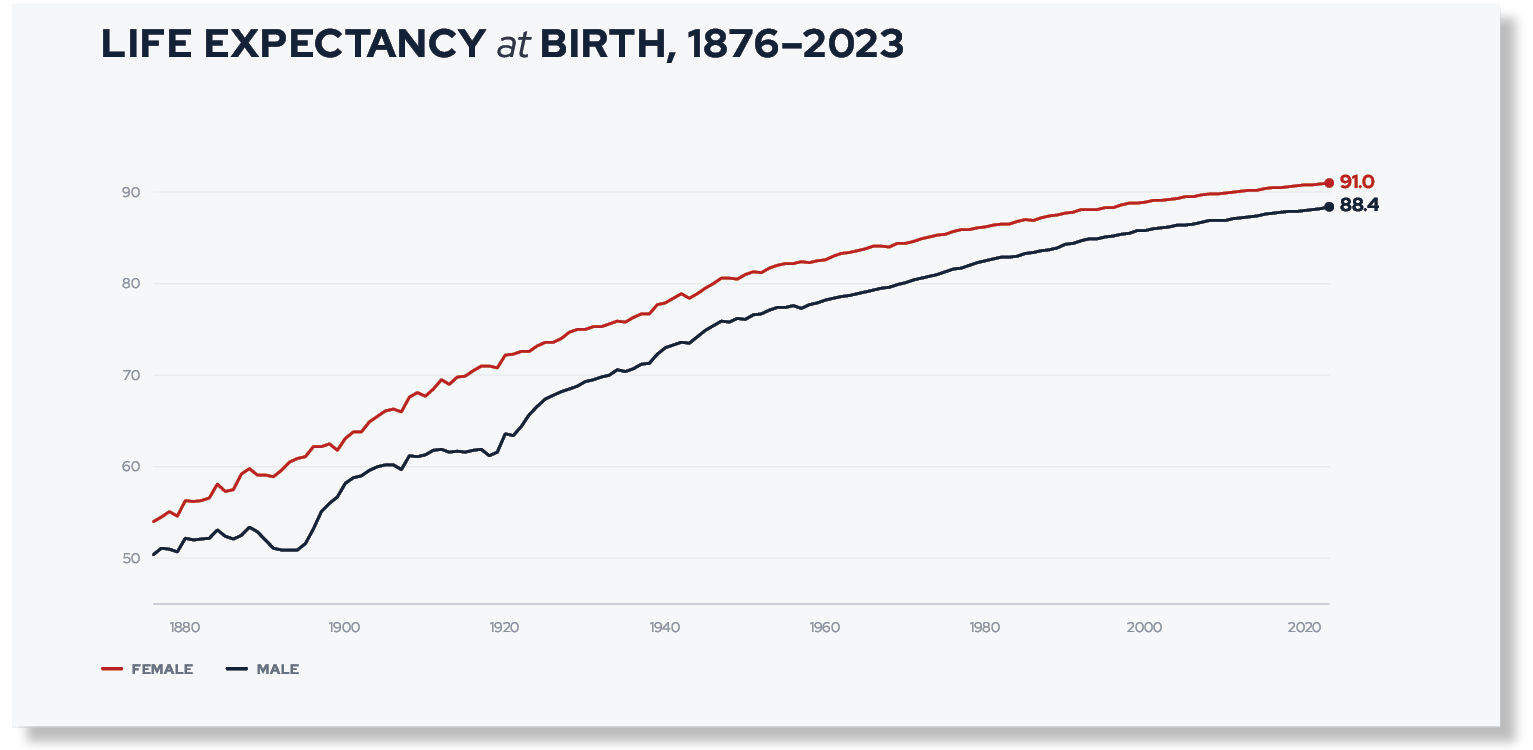

For most of human existence, 50 was the end of the road. In 1900, life expectancy for men in New Zealand sat in the late fifties [1]. A man of 50 in those days really was winding down, because he was nearly done. The Victorians built their whole idea of a life stage around it - you worked until your body gave out, and the gap between the two was mercifully short. Today, a healthy 50-year-old can reasonably expect another 35 years or more, and an increasing number of us will see ninety [1]. We’ve held on to the old instinct that 50 is the beginning of the end, while living an entirely different reality. The body tells us we have arrived. The maths tells us we are barely halfway.

Source data: New Zealand cohort life tables: March 2025 update | Stats NZ

This is where I see good people stumble, though rarely through recklessness. The kids are nearly gone, the mortgage is finally in retreat, and “finally” becomes the word of the moment. Finally, we can do a few things for ourselves! The bucket list, the holidays, the trips deferred for 20 years while school fees and braces and first cars ate every spare dollar. It feels earned, and it feels good, because it is and it does. Behavioural research calls this ‘present bias’; a hard-wired habit of overweighting the reward we can have today against the one we must wait for [2]. But that freed-up cash flow is being enjoyed at the precise moment it should be doing its hardest work. The next 15 years from 50 are prime accumulation time, not the victory lap people imagine them to be.

Most balance sheets tend to be the same at 50: top-heavy with lifestyle assets. The house, the cars, the bach with its rates, maintenance and insurance quietly eroding spare cash or savings each year. It has been the Kiwi dream for as long as I can remember, and there is nothing wrong with wanting that dream. But while the numbers look perfectly reasonable on the surface, the cash flow underneath is poor. The assets that produce real income and liquidity - the ones that will still pay you when your salary stops - are too small to move the needle in this scenario. You’re carrying a great deal of weight that does not work for you, and worse – it's costing you to hold it.

This is where knowing values is crucial. At 50, you need to be clear on what matters and what you must build over the next fifteen years – because every goal is built on cash flow, and cash flow comes from the assets you have accumulated. Get the values right and the rest follows in a straight line. Leave them vague and you’ll inevitably keep spending on what feels good now, instead of what carries you through your 70s, 80s and 90s. The order in which your returns arrive in the early retirement years can make or break a 30-year drawdown, and a poor first few years while you are drawing down does damage that a good average return never quite repairs [3].

It can feel uncomfortable to take such a frank look at your present and future, but it’s fairly straightforward. Do your lifestyle assets fit what you are trying to build? Are you protecting your peak earning stream as the engine that funds everything else? Is your cash flow working backwards, servicing debt on things that do not compound, or forwards, building assets that do?

The gap between what New Zealanders expect to retire on and what they have set aside remains stubbornly wide. It widens fastest for those who assume there is still plenty of time [4]. At 50, most people can still materially change their later years by engaging and making a few incremental course adjustments. These changes don’t have to be dramatic, but they do need to be early. A small correction to a flight path early in the journey lands you in a completely different place.

Often, the best co-pilot on such a journey is a professional financial advisor. And if you think professional advice is expensive, try using an amateur – see what it costs you. Unfortunately, the most expensive amateur you can ever hire is usually yourself; timing the market with optimism and a spreadsheet doesn’t tend to get the same results as methodical, proven strategies and a steady pair of hands at the wheel. Time in the market is the one advantage you cannot buy back later at any price [5].

This is the fiduciary truth of it, and it is the part I care about most after 26 years. Seeking wise counsel at 50 is not an admission of weakness. It’s the best way to understand your own position; we’re all the worst judges of our own blind spots, but an unbiased third party can see the whole scene with clarity.

A good adviser is not there to take the holidays away. They are there to make sure the holidays at 70 are still possible.

50 is the inflection point where you can still move the dial in a way you simply cannot at 65. The runway is shorter than it was, but you’ve got a good bit of tarmac left before earnings come to a stop. The question is not whether the time for preparation has passed (it hasn’t), but whether you will use what remains of it. A burden shared is a burden halved.

Nick Stewart

(Ngāi Tahu, Ngāti Huirapa, Ngāti Māmoe,

Ngāti Waitaha)

Financial Adviser and CEO at Stewart Group

Stewart Group is a Hawke's Bay and Wellington based CEFEX & BCorp certified financial planning and advisory firm providing personal fiduciary services, Wealth Management, Risk Insurance & KiwiSaver scheme solutions.

The information provided, or any opinions expressed in this article, are of a general nature only and should not be construed or relied on as a recommendation to invest in a financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any financial decisions. A disclosure statement can be obtained free of charge by calling 0800 878 961 or visit our website, www.stewartgroup.co.nz

We do not hold or advise on any private credit or private equity investments.

REFERENCES

Stats NZ. (n.d.). Life expectancy. https://www.stats.govt.nz/information-releases/new-zealand-cohort-life-tables-march-2025-update/

ScienceInsights. (n.d.). What is present bias? How it shapes your decisions. https://scienceinsights.org/what-is-present-bias-how-it-shapes-your-decisions/

Sequence of returns risk: Why the order of returns matters in retirement. The Long Math. https://www.thelongmath.com/articles/investing-and-financial-literacy/sequence-of-returns-risk/

Te Ara Ahunga Ora. (2022). Annual report 2022. https://assets.retirement.govt.nz/public/Uploads/Annual-Report/TAAO-RC-Annual-Report-2022.pdf

Dai, W., & Dong, A. (2023, October 31). We found 30 timing strategies that “worked”—and 690 that didn't. Dimensional Fund Advisors. https://www.dimensional.com/sg-en/insights/we-found-30-timing-strategies-that-worked-and-690-that-didnt